With the current health and economic environments seemingly in a constant state of flux as of late, we thought we would share a helpful market update and excerpt from our recent client notice. Kindly note that the data in this commentary is as of April 30th and should be read as such. Our investment team is available to expound on any of the topics covered in this commentary or market events that may have occurred since the time of the writing.

Equity Market Recap

We mentioned in our prior update that the S&P 500, down -19.0% from its highs as of the close on March 11th, was “technically” not yet in a bear market. Unfortunately that comment remained valid for less than 24 hours, as on March 12th the S&P 500 entered a bear market in dramatic fashion, with stocks falling -9.5% on the day. Markets continued to move lower over the next several sessions, which on March 16th saw the S&P post its largest one-day decline in recent memory (and third largest ever, the others being in 1987 and 1929) after falling –12.0%. As of the close on March 23rd the market had declined -34.0% in just 23 trading days.

However March 23rd was to be the bottom, as the next day marked the beginning of a major rally that has seen the S&P 500 gain more than 30% to end April only 14% off its February highs. This rally can be attributed to a combination of factors:

- While equity valuations certainly needed to price in the impact of COVID-19, this is truly a unique situation with many unknowns. In response to these unknowns it appears that many investors adopted a “sell first, ask questions later” approach which in many ways is understandable. So although we can’t say for certain that this will ultimately be the case, the market may have sold off too much, too fast.

- A combination of monetary and fiscal stimulus efforts designed to ensure well-functioning markets and support the economy. The Federal Reserve has taken a number of aggressive actions that have been received positively by investors, while the government passed the massive Coronavirus Aid, Relief, and Economic Security Act (CARES Act).

- Positive news on the virus front, with a deceleration of new cases suggesting the lockdowns/quarantines worked in stemming the outbreak. This allowed for discussion on how to reopen areas of the US at least on a limited basis. Additionally, developments with respect to potential treatments for infected patients have created some optimism.

Fixed Income Market Recap

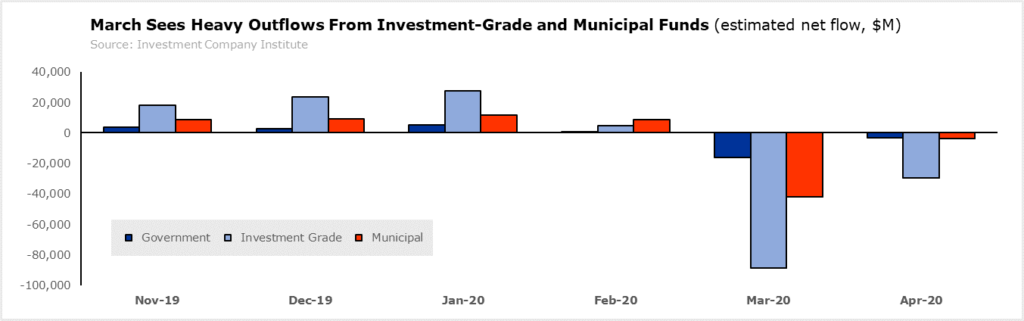

While stocks garnered a majority of the headlines, the fixed income markets were subject to extraordinarily high levels of volatility during the March/April timeframe, and the potential for major dislocations in the credit markets as a result of the COVID-19 outbreak was actually the main culprit sending equity prices lower at times. When the implications of the pandemic for economic and business activity started to become apparent we saw investors look to exit credit-sensitive fixed income assets; this is referred to as a “flight-to-safety” trade which is typical in periods where risk sentiment becomes particularly acute. This time however investors apparently decided to collectively expand their definition of risky assets, and the “flight-to-safety” trade evolved into a “sell-everything-that-is-not-a-US-Treasury” trade.

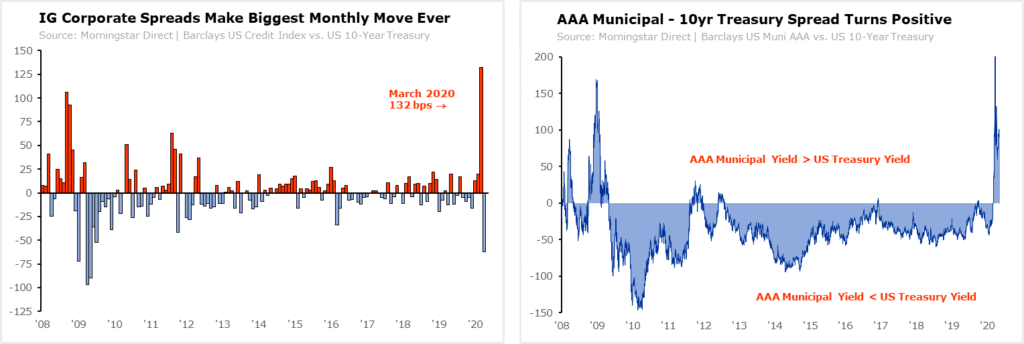

This had a number of ramifications for the markets. Investment-grade corporate bond spreads (the excess yield provided by corporate bonds relative to Treasuries) widened significantly as prices fell, which saw the Barclays US Credit Index decline by nearly -15%. High-quality municipal bonds, typically thought to be one of the safer instruments within the asset class, were not spared as the AAA Municipal – 10yr Treasury spread rocketed into positive territory (AAA municipals typically trade at lower yields than US Treasuries given the tax-exempt nature of the income they provide).

By the end of April bond prices had recovered a majority of their losses, with spread tightening driven by many of the factors that have buoyed the equity market. However we would emphasize that the Federal Reserve played a central role in calming the various fixed income sectors through a range of policy actions, with the major ones being:

- 3/15 – Announces 100 bps rate cut to lower the Federal Funds target rate to 0-0.25%.

- 3/18 – Establishes facility to ensure money markets continue to function properly.

- 3/23 – Expands originally announced asset purchases; limit raised from $700B to infinity.

- 3/23 – Creates program to allow for the purchase of corporate bonds.