While there are many relief programs and packages being introduced to Americans as we navigate the pandemic crisis, it is important to understand those that do or do not apply to your personal situation. Not all offerings are favorable, with fine print presenting challenges in the long run. On the other hand, some programs may be just what your family needs to remain stable during these difficult times.

Our team works with many mortgage professionals on behalf of our clients, and the housing industry is certainly a good example of one that has been the recipient of new programs and considerations. Drew Grandi, Regional Sales Leader at Harbor One, recently shared an update on the newly introduced mortgage forbearance programs. If you are considering taking advantage of this program, be sure to read the release below, and feel free to use it as a guide for discussions with your lender:

Mortgage Forbearance Program and Lending Update

Provided by Drew Grandi, HarborOne Mortgage

Since the end of March, most mortgage lenders have offered their clients the option to apply for a “Mortgage Forbearance Program” to help ease some their monthly financial burdens for clients whose income has been impacted by the pandemic. I have had A LOT of calls on this topic the past month! Some of these calls are from clients who have had their income impacted by the pandemic and need help while others are clients who can still afford to make their mortgage payments but are looking into the details of these plans.

So, just what exactly is this Forbearance Program and is it a good idea for me? Let’s take a closer look.

What Is Forbearance? Forbearance is when your mortgage servicer or lender allows you to pause (suspend), or reduce your mortgage payments for a limited period of time. Most lenders are allowing this deferment for up to 3 to 6 months and can be as long as 12 months. However, you are still required to repay any missed or reduced payments and accrued interest in the future. Your personal Credit Score will not be impacted by participating in a forbearance plan. To qualify, most lenders are not requiring proof of hardship outside of verbal or written verification from the borrower.

Pros:

- Prevents Mortgage Lates or Foreclosure on properties where the borrower would not be able to make their mortgage payments

- Most likely a better solution than having a mortgage late on your credit history

Cons

- Ø Cannot Refinance!: Most lenders will NOT let you refinance your current mortgage during the period of this plan. And, once you have repaid the lender your missed payments, you are still at the lender’s discretion as to whether or not they will allow you to refinance your loan

- Ø Lump Sum Payment: Most plans allow for (6) months of deferred payments but require a lump sum payment after Month 6. If a borrower cannot make one monthly payment now, how will they be able to make up six of them at once?

- Adding an extra amount to your monthly payments until the entire skipped amount is repaid can be an option, depending on your lender

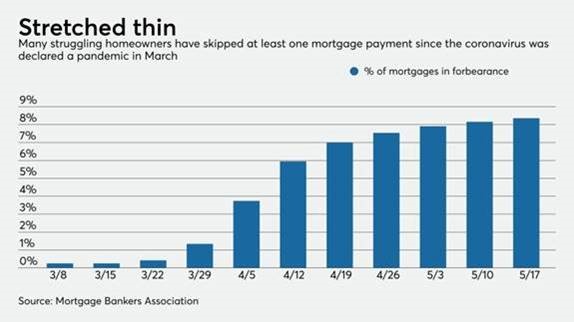

Are People Utilizing this Plan?

According to the latest statistics, nearly 3.5 million mortgages are now in forbearance, amounting to about 6.5% of all American home loans. To put this in perspective, only 0.25% of all loans were in forbearance at the beginning of March. So, I would say that this 25x increase in 2 months indicates that is quite popular with many mortgage holders.

Here is a very informative video explanation by the CFPB about forbearance (4 min.) to send to any of your clients or peers thinking about Forbearance: Forbearance 101 – What it is all about

Summary

In my professional opinion, entering into a Mortgage Forbearance Plan should only be done if you are truly at risk of NOT being able to make your current mortgage payments and need this relief. In this case, I strongly recommend that you put in place a plan to ensure that you will have the savings to repay your missed payments at the end of the plan. People who have had their income reduced due to the pandemic, but can still make their mortgage payments, albeit more painfully, should stay their course and not take the relief. Those of you who are thinking about taking advantage of this opportunity only because it is “convenient” should stay away.

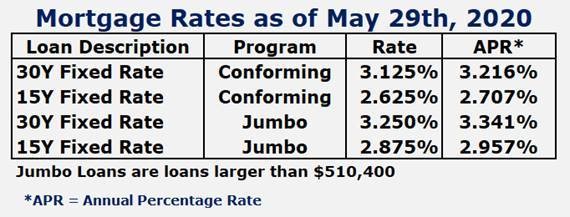

Mortgage Rate Update

I would remiss in my mortgage banking duties if I did not let you know where rates are today for you and your client’s benefit. A little bit higher than last week, but not by much. Below and attached is a quick snapshot of current Interest Rates:

dgrandi@harborone.com l www.loansbydrew.com

The above notice from HarborOne is a helpful overview of the forbearance program, however it is important to note that there may be some particulars unique to your situation that vary from the above information. For example, while some repayment stipulations may require a lump sum to fulfill the obligation of the liability, there are some federally backed loans that offer more flexible options. These include the options to add the amount to existing monthly payments over a set number of months or adding the amount to the end of your loan over the final months. The Consumer Financial Protection Bureau also offers helpful information on relief options. Our financial planning team is available to help Centerpoint clients review any questions they may have regarding the mortgage structure most appropriate for their long-term goals.