Market Update: Back from the Beach, Investors Refocus on Risks

September 8, 2021. By Mark Barry:

As the summer of 2021 draws to a close, we have noticed an uptick in investor unease about the outlook for the economy and financial markets moving forward. Global equity markets remain near all-time highs, but recent events and the headlines associated with them have weighed on investor sentiment. This is occurring at the same time as investors return from their summer vacations and refocus on their portfolios, with the elevated level of uncertainty causing anxiety in the minds of many. In this update we will:

- Review three major “known unknowns” and the potential downside risks they present to the markets; the COVID-19 pandemic, inflationary pressures, and challenges to the economic recovery.

- Examine recent developments with respect to geopolitical risk, US domestic policy, and the potential implications for markets.

- Provide some high-level perspective on the market environment, investing for the long-term, and the approach we are taking here at Centerpoint Advisors in the current climate.

- End with some key takeaways for investors moving forward.

While we lack the requisite crystal ball to confidently and accurately predict the future, we hope that readers will come away with a better understanding of the key issues facing investors today and be more prepared to take periods of market volatility in stride.

As always, the Centerpoint team is here for you; we are always available to talk though any questions or concerns you may have on the markets, your portfolio and financial plan, or anything else currently top of mind, so please don’t hesitate to reach out.

Known Unknowns: Potential Risks and Considerations

COVID-19: State of the Pandemic

The Delta variant has become the dominant strain of the COVID-19 virus in many countries, including here in the United States, where its high transmissibility compared to other mutations has resulted in a new wave of infections. The moderation in growth expectations that occurred in recent months was due primarily to the rapid spread of the Delta variant, which has called into question the sustainability of the economic recovery if aggressive mitigation measures are reimplemented. While financial markets have been relatively sanguine about the variant and associated developments, we have seen a marked deterioration in consumer confidence:

In recent weeks we have seen companies delay employees’ return to the office, venues cancel conventions and concerts, and mask mandates reintroduced. The scenarios for the return of in-person school for children in many districts and locales remains in flux, creating uncertainty for working parents and kids. The media certainly isn’t downplaying the new outbreak either, garnering attention (and ad revenue) with omnipresent headlines. And so it is understandable that consumer confidence has taken a hit, which is reflected in reopening indicators such as bookings for domestic air travel and restaurant visits. Optimism was high among Americans for a return to normalcy as spring turned to summer, but at this point I’m sure many are starting to feel a little too much like Bill Murray in “Groundhog Day” (Groundhog Year: Pandemic Edition?).

Benjamin Franklin wrote that “in the world nothing can be said to be certain, except death and taxes” and this is especially true in investing; healthy skepticism and respect for the unknown are key to long-term success. It surely also applies to evaluating something as new and unpredictable as the COVID-19 pandemic, which has humbled many “experts” in their predictions and seen trust in societal institutions and information sources fall to new lows. At Centerpoint we will continue to maintain a healthy appreciation for “what we don’t know” and that assuredly includes the trajectory of the pandemic. As long-term investors we don’t make major allocation decisions based off short-term expectations or forecasts; with respect to COVID-19 we want to understand the downside risks under a variety of potential scenarios and try to ensure our portfolios are positioned to weather any short-term volatility that arises as a result in order to keep you invested for the long-term. Unfortunately the potential downside risks posed by the pandemic remain both numerous and significant, and we will highlight some of the more obvious ones that investors may have to face in the coming months.

With that caveat, lets start with the upside case. I would suggest the possibility that there may be reason for some optimism, or at least more than the headlines would indicate. Regrettably, it appears that COVID-19 is unlikely to disappear; if that is indeed the case then a realistic goal for a return to “normal” conditions could be a drop in severe outcomes to manageable levels (maybe similar to a bad flu season?). Vaccines appear to be largely effective in reducing severe outcomes of the virus and global vaccination rates are on the rise, while new therapeutics under development have shown promise (Merck’s Molunupiravir which just started Phase III trials is one example; FDA approval of an effective therapeutic would be a gamechanger). And while the scientific community is still working towards a more comprehensive understanding of the Delta variant, the data published to date doesn’t appear to suggest the variant is transparently more deadly and maybe it actually turns out to be less deadly as data from the UK suggests (fingers crossed). The UK experience with Delta also saw infection curves peak sooner than in prior waves, which we may be seeing in the US. Below is a chart illustrating hospitalization curves for the pandemic in the United States where we see a tentative peak in hospitalizations and the beginning of what is hopefully a sustained downward trend.

I would reiterate again that we are maintaining a healthy respect for the unknown here; the future path of the COVID-19 pandemic is highly uncertain, and we have zero confidence in our ability to forecast its impact on the markets and the economy to any degree of accuracy. With the help of their advisors, investors need to keep emotions in check and maintain their strategy discipline, understand the various risk scenarios, and focus on the long-term. The last two years have been a challenge in this respect, and there is a growing sense of frustration as the pandemic drags on and more aggressive mitigation measures return. Exacerbating this frustration, in my view, is the fact that many institutions and policymakers lack any sort of coherent, realistic, or achievable strategy for dealing with the virus and too often pursue reactive policies in pursuit of undefined goals, which is disappointing at this stage of the pandemic taking all things into consideration. Hopefully we see a little more cost-benefit analysis incorporated into decision-making moving forward as the world attempts to manage the implications of the virus on public health, economic growth, and overall wellbeing.

Now lets turn to the potential virus-related risks, which as noted are substantial. For the financial markets, the key issue is the extent that infection outbreaks cause governments and private institutions to implement more aggressive measures to reduce spread that negatively impact the reopening of world economies. Below we have outlined some potential risks and/or downside scenarios:

- Current outbreak is not peaking; infection rate rises in northern US states in fall / early winter. Southern states hit harder during summer months (spend more time in air conditioned indoors) and northern states may see another wave with the return of colder weather (more time indoors).

- COVID-19 expands and/or mutates into a more virulent and deadly virus, potentially one that poses more risks to children and those otherwise young and healthy. Some evidence suggest Delta variant may be worse for children/younger people. Lockdowns implemented to protect children.

- Vaccine efficacy is further called into question. Vaccines appear to be working well but some evidence of declining protection with time. Already confusion with respect to booster shots. See situation in Israel.

- Pandemic drags on at current level; some state and local governments continue with periodic lockdowns and/or restrictions which hinders economic activity and stunts recovery in consumer spending. Schools do not return to full-time in-person learning which impacts labor market. Supply chain bottlenecks for many goods don’t abate causing combination of shortages and goods inflation.

These risks will remain top of mind for investors and if realized in some form would likely trigger a correction in the markets, the degree of which would depend on the severity of the developments. We will continue to closely monitor the trajectory, impact, downside scenarios, and potential future risks of the COVID-19 pandemic, but as long-term investors will focus on our investment discipline and strategy which is under our control.

Inflation, Fed Policy, and Treasury Yields

The Consumer Price Index (CPI) rose 0.5% in July, with prices increasing 5.4% year-over-year. US inflation is now running at a 7.1% annualized rate in 2021. For some components of CPI such as durable goods, price inflation to a significant degree can be attributed to temporary factors such as COVID-19 induced supply chain issues (see the backup at the two largest ports in the country). These factors should moderate and eventually resolve themselves which would alleviate inflationary pressures to some extent. However, there are also signs that inflation continues to gain momentum; for example, wages (which tend to be “sticky”) are rising at a 4% pace on the year. Food, energy, and housing prices have all risen meaningfully over the past two years and given their weight in average household budgets could crowd out discretionary spending should they continue to rise.

The Federal Reserve has continued to express the view that inflation is “transitory” and will return to its 2% annual target in short order. Price stability is one half of the Federal Reserve’s dual mandate, the other being maximum employment. With the recovery in the jobs market having a long way to go and inflation continuing to exceed expectations, Fed Chair Jerome Powell has to walk a bit of a tightrope in terms of policymaking:

- Should the Federal Reserve tighten monetary policy in an effort to combat inflation and economic activity proves weaker than expected, we could see the recovery stall and deflationary risks increase.

- If employment proves to be the Federal Reserve’s primary focus and they wait to see further job gains before tightening policy, they may lose control of inflation and risk overheating the economy.

We do not have a strong conviction as to the future path of the economic recovery nor where inflation is headed. However, given the unprecedented level of fiscal and monetary stimulus that has been pumped into the economy in response to the COVID-19 pandemic (and an additional $4.7 trillion in new spending currently under consideration in Congress), we view a sustained and rapid rise in inflation as a potential downside risk that may currently be underappreciated by investors. If 10-year Treasury yields grind towards 2.0-2.25% in the coming quarters the markets might be able to handle that just fine, but if we get a disorderly rise in yields to those levels or higher, the equity markets would likely see significant volatility.

Investor Complacency RE: Economic Recovery

Even if one takes an optimistic view of the future path of the COVID-19 pandemic, it still seems to us that there is a bit too much complacency in the markets with respect to the economic recovery. Many risk assets (stocks, high yield bonds, etc) appear priced to perfection, so evidence of slowing economic activity or new economic pain points materializing may necessitate a rerating and disrupt the trend of steady appreciation we have seen. The specific risks here span a wide spectrum but below are a few items we will be watching:

- The past month has seen some weaker economic data out of the US, with retail sales, housing starts, and existing home sales all disappointing. This was not entirely unexpected after a period of strong growth, and we can attribute at least some of this weakness to the Delta variant, labor market constraints, and surging home prices. US economic indicators remain broadly positive, but should a deteriorating trend become apparent markets would have to revise their rather rosy assessment for growth downwards.

- Chinese economic data also surprised to the downside in August, with both manufacturing and services sector PMIs showing a contraction. A weaker-than-expected Chinese economy would pressure global growth.

- The state of the US jobs market is also a bit perplexing; companies are struggling to hire, with US job openings at a record high of 10.1 million. Yet the unemployment rate remains elevated at 5.4% and more than 6 million jobs lost as a result virus-induced lockdowns have yet to be replaced. Not exactly sure what is driving this disconnect (could be a mix of several factors), but ideally it resolves itself in due time.

- Supply chain bottlenecks as noted earlier are causing price inflation in certain goods, but there is a risk that these take longer to work through. The semiconductor shortage continues to extend its timeline which has seen ripple effects across the economy; for example, automakers including GM, Ford, Toyota, and BMW have announced production shutdowns due to lack of semiconductors used in their vehicles which results in lost income for their production workers while also driving new and used auto prices higher.

Recent Events: Geopolitical Risk, US Domestic Policy, and Potential Implications for Markets

China: Regulatory Landscape and US-China Relations

Recent months have seen Beijing target many large publicly listed Chinese companies with aggressive regulatory action, issuing directives that kneecapped several businesses along with their share prices. Didi Chuxing (the Chinese version of Uber) was the first in the crosshairs; on June 30th the company IPO’d on the NYSE and traded for two days before China banned their platform from app stores and announced an investigation into the company. The rest of China’s technology giants received similar treatment, as did the for-profit education sector.

Without going into too much detail, the overarching objective of this crackdown appears to be forcing alignment of the corporate sector with Chinese policymakers’ economic, social, and security priorities which are not always easy for Western observers to discern. And an effort by President Xi Jinping to further consolidate power in the run up to his 10th year as the country’s leader may also factor into the crackdown to some extent, as it has provided the opportunity to purge potential rivals in the business community (the billionaire founders/owners) that have become quite powerful in their own right.

Given that these Chinese stocks are listed on American exchanges and US investors make up a sizeable amount of the shareholder base (and were disadvantaged here), the SEC is not standing idle. This recent episode was a wakeup call for many foreign investors who have begun to appreciate the potential for continued decoupling in the US-China relationship, which was under strain prior to 2020 but has only become increasingly so with the COVID-19 pandemic and China’s “wolf warrior” approach to international diplomacy. From what we have seen, Wall Street has largely been rationalizing this risk away (can’t put that China M&A revenue in jeopardy . . .) and is now recommending sectors viewed as less likely to be targeted by the Chinese government to their clients. It remains to be seen how the relationship between the US and China progresses moving forward, but at present seems unlikely to improve significantly in the near-term and carries downside risks to the markets should relations deteriorate further in a meaningful way.

Afghanistan Fallout

At first glance America’s humiliating evacuation from Afghanistan would appear to have few implications for the economy and financial markets; American’s were broadly in favor of a withdrawal and the country hasn’t exactly been a hot destination for private capital in recent years. The execution of the withdrawal however was an outright disaster and made the United States look grossly incompetent at a minimum (among other consequences). This certainly didn’t positively impact the psyche and optimism of the average American investor to say the least, and may filter down and impact the economy and markets in a couple of ways:

- Introduces more geopolitical risk, as hostile actors (such as Iran, Russia, North Korea) may seek to exploit the United States’ perceived weakness and test the administration. Raises questions about outcome in the event of a major foreign policy crisis in the future.

- Potentially further imperils President Biden’s domestic policy agenda, which had already somewhat stalled in Congress. Two bills that propose more than $4.5 trillion in new spending are priority items on the list, and the events in Afghanistan will likely erode support at the margins, particularly from Congressmembers in purple districts as they look towards the 2022 midterms. It is unclear how much of this fiscal stimulus is currently priced into the markets (probably some, but not all), but if the eventual number is outside of expectations the markets would have to incorporate the direction of the surprise into prices.

Policy Developments: Infrastructure and Reconciliation Bills

The House is expected to vote sometime this fall on the $1.2 trillion bipartisan infrastructure package passed by the Senate. The passage of the bill would be welcomed by the financial markets as it includes investments in various infrastructure projects such as roads, bridges, airports, and waterways that would be beneficial to the economy. We would guess that the infrastructure bill eventually gets passed in one form or another, but this could take longer than expected given intraparty disagreement over efforts to tie its passage to a contentious $3.5 trillion spending package that is also moving through the legislature, and of course the rank partisanship that has come to be associated with Washington. This $3.5 trillion bill appears to have a more challenging path than the $1.2 trillion infrastructure package, and at present does not have the 50 votes needed to clear the Senate through budget reconciliation. Given the amount of new spending the bill would inject into the economy it is something the markets are watching. Below are some brief highlights/notes on the policy and legislative outlook that warrant investor consideration:

- The House passed the $3.5 trillion budget resolution on August 24th. This resolution instructs various committees to develop policy proposals for inclusion in a reconciliation bill (there is no actual bill yet).

- A House Budget Committee report communicated that “This Plan will be paid for by ensuring that the wealthy and big corporations are paying their fair share.” Top priorities are a) raising the corporate rate to 25% or higher, raising the top individual marginal rate to 39.6%, and raising the capital gains tax rate to 28% or higher per commentary from GrantThorton.

- As it stands it appears unlikely that the $3.5 trillion bill will be passed as is and will probably have to be watered down significantly to get all 50 Senate Democrats on board; there are at least two Democratic Senators who have already signaled their opposition to that level of spending, with its impact on inflation and the national debt cited as major concerns.

- One potential scenario could be an extended period of political gridlock as these bills are held up by general partisan disagreement and the volume of amendments particularly by members from swing districts/states up for reelection in 2022. Should economic data deteriorate for any reason (COVID-19 lockdowns would be a big one) and/or the equity markets experience a correction/volatility, this could spur Congress to agree on a compromise or a new stimulus bill in order to be seen as “responding” to the adverse developments.

- Amidst these spending fights there is also the potential for another government shutdown with an October 1st deadline for additional government spending legislation. In 2011 this resulted in the United States sovereign credit rating getting downgraded by a notch leading to an equity market selloff.

- On the other hand, markets could be underestimating the size of the combined spending that ultimately gets passed, which would be an upside surprise stocks might react favorably to.

Perspective On the Current Market Environment and Our Approach

While the current environment may seem especially uncertain given the potential risks outlined above, we still view the fundamental backdrop for equities as positive. Second quarter earnings proved to be exceptionally strong, US economic activity remains robust, and there are several potential upside catalysts (improving COVID-19 environment, an infrastructure bill, corporate buybacks, etc) that if realized would support continued gains. That said, investor return expectations need to be set very modestly as equity market valuations are meaningfully above their long-term averages.

Trading at elevated valuations however doesn’t necessarily make the market too expensive to see further appreciation but does make it more likely that investors must endure volatility and pullbacks along the way. We understand it can be difficult to stomach short-term market volatility and periods of steep declines, but these are a normal part of the market cycle. Investors who can maintain their investment discipline through bouts of market weakness will likely be rewarded in the long run over which the equity markets and other risk assets have proved to be excellent vehicles for investors to allocate capital.

Market Corrections Happen

A market correction is defined as a drawdown of -10% or more from peak to trough, and historically these occur about once per year. The US equity markets last experienced a correction in February/March 2020 as the COVID-19 pandemic hit (which was also technically a bear market as the drawdown exceeded -20%) and have marched steadily higher for the most part ever since. We are probably overdue for a correction or at least a healthy pullback at some point; while we cannot forecast when it will happen – it could be in a week, a month, a year, or more – we can almost guarantee it will happen eventually.

Given that it is almost impossible to time the market consistently with any degree of accuracy, investors should be prepared to sit tight and avoid making emotional decisions when volatility resurfaces. It is important to realize that corrections – and to an extent even bear markets – are not rare events.

Stocks Will Reward Investors in The Long Run

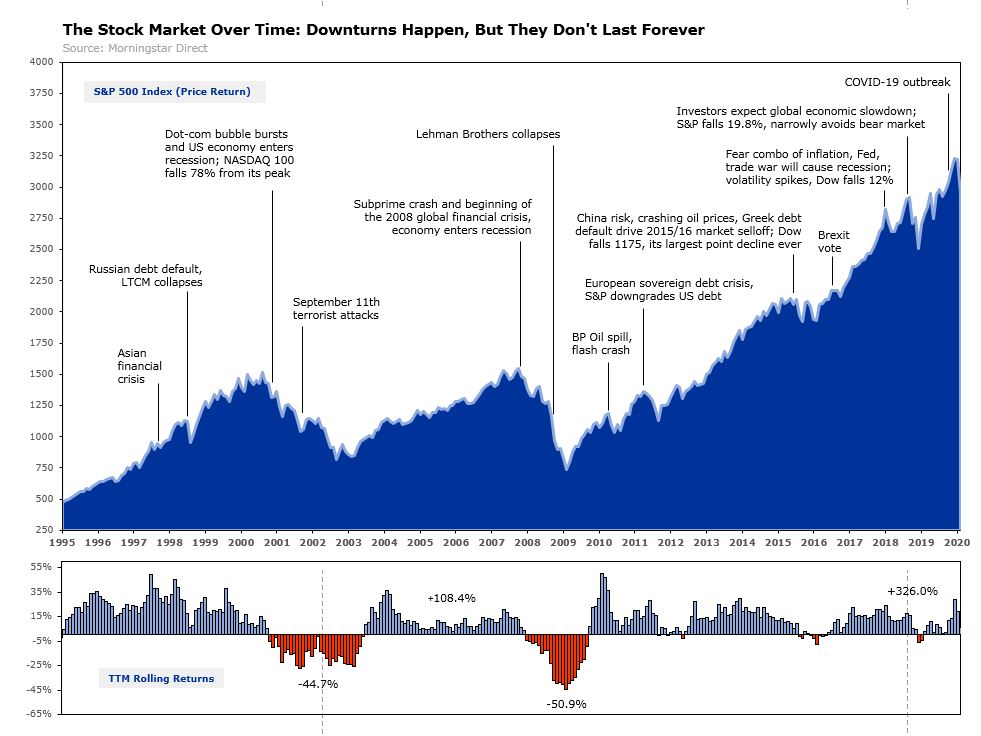

We know that the long-term trend of the stock market is up, and that timing the market in the short-term is a difficult if not impossible task for most (one of the reasons we often dollar-cost average). Fear and greed are powerful emotions however and can cause investors to eschew logic in their decision making. We understand how nerve-wracking it can be when volatility picks up and markets come under pressure, but we encourage investors to maintain a long-term perspective. Over time the market tends to climb the “wall of worry” and eventually manages to move past negative events no matter how serious they are; in previous updates we have included our market timeline chart which we think illustrates this point well.

{kind=link}

In this update however we will change things up and share a different supporting example. Below is a chart of the 5-year trailing returns for the S&P 500 Index since 1941. Basically, there is a data point for each month expressed as a blue or red bar on the plot, and that data point is the annualized return of the US stock market (as represented by the S&P 500 Index) for the prior five years. We would highlight that:

- Periods with positive five-year trailing returns (in blue) are significantly more prevalent than those with a negative return (in red). If you picked a random month to invest in the stock market between 1941 and 2016, there is a 91.5% chance you would have experienced a positive annualized return five years later.

- If we extend the time period to 10 years, the probability of a positive return moves to 97.3% (and the 2.3% of five-year periods that were negative all assumed that you invested during the 1999/2000 tech bubble and sold following 2008/2009 financial crisis or thereabouts).

- The magnitude of the absolute values of five-year positive returns compared to the negative ones is also worth noting; there are lengthy periods of strong positive returns, and you want to stay invested in order to avoid missing these bull markets which drive long-term performance.

The bottom line is that equities remain an excellent investment option for generating long-term real returns, and we believe they warrant an allocation in most investor portfolios. It is true that past performance is no guarantee of future returns, but if history is our guide the prospects for the long run look good. There is always the chance of a “Lost Decade” in the stock market, such as that which was experienced from 2000 to 2010, but this has not been a frequent occurrence in modern history. Even then given enough time the trend for stocks has been upwards and to the right on the growth chart.

How Centerpoint is Approaching Things

At Centerpoint Advisors we will continue to maintain our discipline in the design and execution of investment strategy. While we will adjust our positioning at the margins based on the current market environment, we don’t believe in making allocation decisions that are predicated on short-term expectations or forecasts. Instead, our aim is to construct durable portfolios that will keep you invested through periods of market volatility and achieve the specific goals that your allocations were designed to target; portfolios that are tailored not only to your financial plan but to your unique needs and perspectives as well.

We feel that a well-diversified, durable portfolio combined with a long-term view is the best way to manage through uncertain environments like the one we find ourselves in today. As your advisor we will always be monitoring the potential risks in an effort to assess the range and probability of various scenarios over shorter time horizons, but investment decision-making will remain centered on the long-term which is key for investment success.

Given the healthy valuations that many risk assets currently sport, we have generally been advising clients with new monies targeted for these allocations to invest on a systematic monthly basis. With equities near all-time highs after a strong run of performance we are paying close attention to the allocation mix of client portfolios; recent appreciation may have caused equity exposure to drift outside allocation guidelines and thus in many cases warrants a rebalance to bring portfolio risk levels back within an acceptable range. We will be conducting rebalancing actions for tax-exempt accounts as we move into the final quarter of the year, while assessing all of our taxable portfolios for rebalancing needs in consideration with potential capital gains implications. As always, we will reach out to you prior to executing any rebalancing trades that would realize material gains.

To briefly review our current portfolio positioning from a high-level, our equity allocations remain diversified across the large, mid, and small cap styles with exposure to both US and international markets. Within this allocation we maintain a modest overweight to “Quality” stocks which gives us a slightly more defensive posture from a valuation standpoint. On the fixed income side, we remain conservatively positioned from a duration (interest rate) standpoint. In recent months we took advantage of the sharp decline in Treasury yields to reduce our exposure to the intermediate part of the yield curve and introduce a small allocation to an alternative income strategy which has enhanced our bond portfolios from a yield and diversification perspective. We continue to evaluate additional investment opportunities for inclusion into our portfolios that offer what we view as an attractive risk/return tradeoff in this relatively challenging environment.

Key Takeaways for Investors

After reading this update we hope that investors will be broadly cognizant of some of the potential risks faced by the economy and financial markets while also gaining perspective that will enable them to stick with their investment strategy and remain disciplined when the waters eventually turn choppy. And as illustrated, they inevitably do. In closing, we want to reiterate three key takeaways for investors:

- Maintain a long-term perspective; take short-term market fluctuations in stride and know that your portfolio is constructed for success in the long-term with your goals in mind.

- Don’t let emotions drive decision-making; remember that corrections are not rare events, volatility is part of the normal market cycle, and stocks have historically rewarded investors in the long-run.

- The Centerpoint team is here for you; we realize that staying the course can be uncomfortable when markets are enduring declines. We are always available to talk though any questions or concerns you may have on the markets, your portfolio and financial plan, or anything else currently top of mind.