November 22, 2016. By Courtney Faria:

Retirement seems a long way off for many millennials. Some have just entered college, or are just entering the workforce, like me. Others are getting married and starting a family. So many changes and adventures are ahead; some exciting and exhilarating, yet some causing great stress. While balancing so many important day-to-day items, retirement is rarely in the forefront for these millennials, despite concerns about the government’s ability to continue funding Social Security. Why is that?

Most millennials (those born between 1980-2000) have vivid memories of the Dot Com bubble, the financial crisis of 2008 and its accompanying housing crisis, watching their family’s assets and securities diminish along the way. Given this experience, it is easy to see why this group tends to have a more conservative approach with money. According to an analysis by State Street and a survey conducted by UBS, millennials hold significant amount of their portfolios in cash, around 40%; while non-millennials hold less than a quarter in cash. These investing actions, or rather, non-investing actions, have been compared to those of young adults during the great depression. The minimal confidence in the markets, paired with distrust in financial professionals, results in the millennials’ viewpoint that investing in the market is a risk not worth taking.

Fear of loss of capital is prominent, but is not the only driver behind the lack of millennial investment. The minimal confidence in the market does not only stem from growing up during a time of recession, but also from a severe lack of financial literacy. Complex jargon and negative media coverage leave millennials less assured about investing in the market because they simply don’t understand how a diversified portfolio works. State Street had members from the millennial, gen X, and baby boomer generations participate in a basic financial literacy test. Those from generation X and baby boomers scored 57% and 65% respectively, while millennials scored less than 50%. Despite the fact that they acknowledge this illiteracy, millennials are the largest consumers of do-it-yourself investing technology such as robo-advisors. The cost sensitivity is attractive, however what this generation really needs is the education and financial coaching that can best be provided by a professional advisor.[i]

Financial obstacles, mainly student debt, also prevent millennials from investing their hard-earned money. With student debt on the rise each year, and tuition rates increasing at 6% per year, young adults have less disposable income for retirement savings. In extreme, yet common, cases this increase in debt causes them to move back in, or continue living with, their parents- a phenomenon leading to a separate set of domestic macro-economic consequences. In conjunction, employment levels are barely escaping the prerecession standards making it difficult for graduates to obtain a job with a salary high enough to cover loan payments. By the time solid careers are established investing in the company’s 401(k) unfortunately doesn’t seem like an immediate necessity, even if it should.

This combination of conservative mentality, financial illiteracy, and financial obstacles are hindering the ability to take advantage of tax-deferred investing and professional management. After all is said and done, however, millennials are in fact curious about investing. If you fall into this category, we encourage you to speak with a fiduciary financial professional. Here are some tips to consider while you are preparing to enter the market:

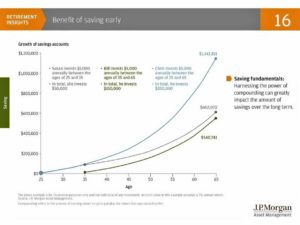

- Start now. Every little bit counts when saving for retirement to capitalize on the benefits of compounding.

The earlier you start saving the better

If your company offers a retirement plan, such as a 401k plan, start now and try your best to meet any match that may be offered. It is perfectly fine if you can only afford to put in a small amount, but it is important to start somewhere; you can always dial up the volume when you feel comfortable. An investment advisor can assist with your investment options and can help allocate your contributions into investment vehicles that are geared to your ultimate goal.

- Mutual funds may be a good option to diversify your money across a number of different stocks and/or bonds, which reduce the concentration risk, i.e. risk of putting all your eggs in one basket. In addition, mutual funds are commonly offered in 401(k) or other employer sponsored plans. ETFs, or Exchange Traded Funds, may be another option to diversify at a lower cost. Consult a financial professional before investing to ensure that investment vehicles and their fee structures are appropriate for your risk tolerance and investment objective, as not all mutual funds and ETF’s are designed alike.

- Thanks to web-based efficiencies, many advisors now pair technology with customized advice to maximize your time and increase transparency. Not only will you have online access to your accounts, but you will also have access to a team of professionals who can explain your investments in detail.

- Pay attention to the fees and taxes you pay. An advantage of a 401(k) or other similar retirement plan is that they allow you to make pretax contributions, and taxes are only paid when withdrawing money upon retirement, so all dividends or interest earned that get reinvested into your portfolio can grow tax free until you retire. If your employer does not offer a retirement plan, consider speaking to an investment advisor about other types of retirement accounts that may be available to you, such as an IRA.

- Although the stock market has generally experienced positive returns on average over the long-term, markets can go down, and money can be lost. This is the harsh reality and drives home the importance of risk assessment. Implementing a professional strategy free of behavioral bias can help you weather market downturns. This is yet another advantage of using an investment advisor.

As with most things, it is best to get a head start, especially for retirement, and the classic Benjamin Franklin quote still rings true – “By failing to prepare, you are preparing to fail.”

[i] We urge anyone interested in considering a DIY/robo only strategy to read our recent blog by Richard Greene, “DIY+Robo+Behavioral Bias=Use and Advisor”