March 30, 2017: As summer vacation approaches and acceptance letters begin to appear in your mailbox, use these opportunities to discuss sound financial habits with your teen and young adult children before they are off “on their own”. Here is a great post by John Wolfsberg that is worth sharing again now that spring has arrived:

How to Talk to Your Teen and Young Adult Children About Money

August 9, 2016. By John Wolfsberg:

The teenage years offer many opportunities to open up a discussion about financial responsibility, as children begin their first jobs and increase social activities. Financial coaching, however, extends through and beyond the college years as well; it may not be until they are out on their own that the true nature of their spending or savings habits come to light. As any parent knows, the worrying does not stop just because your children are not under your roof. It can seem awkward to start a conversation about financial responsibility at this stage if you have not already, but unless you plan on keeping the lending division of the Bank of Mom and Dad open for business, it may be necessary. Beginning the conversation during the teenage years will provide an even better foundation.

Various emotional elements can be attached to the topic of money for both the parent and the child. If this is the case, it could be helpful to engage a third party, such as your financial advisor, to have this discussion– not coming from mom or dad, insight may be perceived less like a lecture and more like something valuable to consider. At our firm, we work with many next generation clients to provide objective advice and insight into their spending and savings habits . If you do decide to engage your child in a discussion on finance, you will want to incorporate these suggestions:

Teenagers:

- Keep Track: With college on the horizon, it is important to learn how to create a budget. Figure out what you need each week (be honest with yourself for this part) and stick to it. Before each semester, figure out how much money you will need to earn during breaks to support your term spending. Our College Budget Worksheet can help.

- Parent Bills vs Teenager Bills: Understand which expenses parents are responsible for versus those the teenager is responsible for. If the parent is covering the car insurance and repairs, but the teenager is responsible for the gas, then this arrangement should be adhered to. It is difficult to budget correctly if an expense is paid for some weeks but not others.

- The Cash-Only Diet: Use cash only for a week or two to get a better understanding of your spending habits. Using a debit card for every purchase is convenient, but allows you to blow through a budget quickly. Estimate how much you need each week for spending, take that amount out of the ATM each Sunday afternoon and see how long you can last WITHOUT using the debit card.

- Count the Little Things: Don’t underestimate the cost of small reoccurring purchases. Your double iced espresso latte may be only $3.50 each day, but that’s $24.5 a week and almost $100 a month. Wants and needs are two totally different things.

Young Adults

- Pay Your Savings Bill: Treat your savings account as any other bill and pay it. Think of this as the ‘bill’ you should always pay first. As previously mentioned, calculate a weekly budget. Determine how much you need each week and deposit any excess into a savings account separate of your checking account. As it grows, you can further break this account into buckets such as emergency and long term savings (i.e. something for a future purchase, such as a home). You may then want to consider investing.

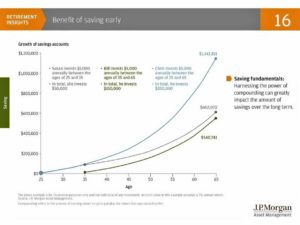

- Time is on Your Side: If you have started a job and it has a retirement plan such as a 401k or 403b, participate in it each pay period, even if it’s just a small amount. Your best friend at this point in your life is TIME (see chart below). The earlier you start saving the better. Once automatic deposit is set up, it’s easy to increase the amount, and if you elect to deposit a percentage rather than a set amount, your contributions will increase as your wages increase, making it easy to stay on track.

The earlier you start saving the better

- Reconcile Regularly: Use an app that allows you to easily reconcile your bank account weekly. Out of sight out of mind is a real phenomenon; visually noting where your money has gone will help to keep long-term goals in mind. Better yet, balance an actual check book. Exposing your children to their own bank accounts and teaching them the ins-and-outs of deposits, lag time, and fees can begin in the teen years.

- Avoid Excessive Use of Credit Cards: While it is important to have a credit card for EMERGENCY situations, you should avoid excess use. If you do have to use a credit card for an emergency (car repair, etc.) make sure the balance is paid off quickly – do not fall into the trap of making the minimum monthly payment. Beware of introductory offers on retail store cards. Interest rates are high and late fees are out of sight. It is also easy to forget that you have a department store card leading to missed payments. Just one or two missed payments will create late fees and hurt your credit score. If you do use the card, pay it off entirely each month.

Many assumptions are made regarding poor financial habits of millennials, when in fact many are simply stuck trying to dig out from large student loans while at the same time attempting to leave the family home to branch out on their own. We realize our children are in a different environment than the one we grew up in, and know that in many ways it is more difficult for them financially than it was for our generation. On that note, it is important to remember that their experiences are not our own, and some lessons can be learned only from tribulation and not from words. From conversations with my own children I can offer the following advice for your talk: be compassionate, listen well, and avoid sarcasm. Finally, start these conversations early as it is better to establish good financial habits as a teenager than trying to develop them as an adult.