May 23, 2017. By John Wolfsberg:

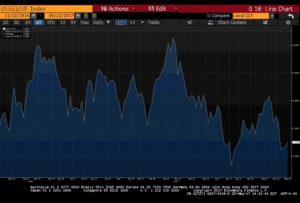

Expectations for higher interest rates increased almost immediately with the election of Donald Trump as our 45th U.S. President. Much of President Trump’s campaign platform focused on major growth initiatives that many felt would result in stronger economic activity, increased national debt (financing of infrastructure) and ultimately higher prices (inflation). Indeed, immediately after the results of the election, equity markets began to rally and interest rates began to move higher. The benchmark 10yr Treasury approached 2.60% in early December (testing this level again in early March) but only to decline back down to the 2.25% level (as of this writing), thereby retracing exactly half of the yield increase since the election results.

(10 Year Treasury Yields in the 6 Months Since Trump Election)

Several factors seem to be weighing on the move lower in rates. The first appears to be investors’ realization that President Trump’s campaign proposals may not be enacted as easily as originally assumed. This became evident when Congress could not agree on a replacement for the Affordable Care Act, the repeal of which President Trump was adamant about throughout his campaign. Investors are now asking themselves, if a Republican controlled congress and White House can’ t agree on healthcare reform, what other campaign proposals are at risk? Infrastructure spending? Tax reform?

Second is a combination of both geopolitical risk and domestic political turmoil. President Trump has made it clear that his policies are focused on “America First”. It’s no surprise that some of his rhetoric and dealings with other countries so far has resulted in flight to safety trading as concern over international relations rises. North Korea has been in the news and continues to pursue a nuclear missile program that is concerning to all. In addition, the formal start of BREXIT has investors concerned that the economic fallout in Europe could be significant. As U.S Treasuries offer attractive yields versus many other developed countries, capital continues to flow into our bonds keeping rates down. President Trump’s domestic political battles are beginning to be a distraction from the agenda he set forth when he took the Presidency.

Finally, while there have been pockets of solid economic data over the last two quarters and labor market data continues to show solid gains, we have seen some interesting soft data as well:

- Recently, housing starts dropped 6.8% month over month. While some argue the decline is weather related, the drop was evident in areas outside of those impacted by storms. Keep in mind that the housing and related sectors account for a significant portion of jobs.

- Inflation data continues to remain subdued with the consumer price index running well below the Fed’s 2% target rate. The conflicting data does not give investors a clear signal that the US economy may be overheating, thus justifying higher rates.

Looking forward, where does this all lead us? The forces impacting interest rates continue to grow and be at odds, making a call on the future direction of interest rates nearly impossible.

Those who expect rates to increase point to an improving economy, an FOMC committed to raising rates, and increased national debt issuance to support spending as their main arguments for higher yields. Conversely, those who argue rates can remain lower cite low inflation, low yields abroad, a divisive political environment, diverging economic data, and major shifts in demographics as some of the reasons that will keep rates low.

Making a call on the direction of interest rates has proven to be difficult (which is a huge understatement), yet one concept is beginning to become clear – the opposing forces impacting interest rates appear to be in balance. Until this relationship moves out of balance (i.e. political or economic issues improve) we are unlikely to see a significant and sustainable move to higher rates.